Key Takeaways:

- Importance of early retirement planning

- Strategies for Maximizing Retirement Savings

- Understanding different retirement account options

- Using realistic projections for retirement income and expenses

- Managing and adjusting plans over time

The Importance of Early Planning

Starting your retirement planning early can make a significant difference in securing your financial future. Taking advantage of retirement planning services early on allows you to benefit from compound interest and manage financial risks better. Many financial advisors agree that early planning can lead to long-term benefits. According to a report from Forbes, the earlier you start, the more you’ll save in the long run.

Moreover, early planning provides a cushion against life’s inevitable financial uncertainties. It gives you the flexibility to adjust your savings strategy as needed. For instance, during significant life events such as marriage, the birth of a child, or sudden changes in employment, having a robust retirement plan can serve as your financial safety net.

Additionally, starting early allows for a longer investment horizon, enabling you to weather market fluctuations more robustly. You have time to recover from downturns and can afford to take more calculated risks, which could yield higher returns.

Maximizing Your Retirement Savings

You need to be strategic and consistent to get the most of your retirement funds. Without the inconvenience of manual transfers, setting up automatic contributions to your retirement accounts guarantees that your savings are steadily growing. This “pay yourself first” approach prioritizes your long-term financial health.

Employer matches are another critical component. Ensure you contribute enough to your retirement account to maximize any matching contribution your company may offer. Since compound interest accrues over time, increasing your donation by even a tiny percentage can have a big impact. That is why it is referred to as “free money.”

Investment selection also plays a crucial role in maximizing retirement savings. Investing in a range of asset classes can lower risk and boost returns. Rather than concentrating all of your assets in one area, a well-diversified portfolio comprising bonds, equities, and other investment vehicles can provide a more consistent growth trajectory.

Financial experts advise routinely assessing and rebalancing your holdings to match your investment portfolio with your risk tolerance and retirement objectives. Rebalancing entails modifying the proportions of various assets to maintain the appropriate amount of risk and return in your portfolio.

Different Retirement Account Options

Retirement accounts come in various forms, each with advantages and tax consequences. Making educated selections can be aided by being aware of your possibilities. Typical accounts consist of:

- 401(k): These accounts, which companies usually provide, allow tax-deferred growth on your contributions and possible company matches. Plans for employee-sponsored 401(k)s frequently offer a range of investment choices, so you can customize your portfolio to match your level of risk tolerance.

- IRA: Individual Retirement Accounts allow for tax-deferred growth and offer various investment choices. IRAs are particularly beneficial if your employer does not offer a retirement plan, allowing you to select investments that suit your retirement goals.

- Roth IRA: Because eligible withdrawals are tax-free and contributions are paid using after-tax money, this option is useful for people who anticipate retiring in a higher tax bracket. There are no minimum distribution requirements with Roth IRAs, so your money can grow tax-free for an extended period.

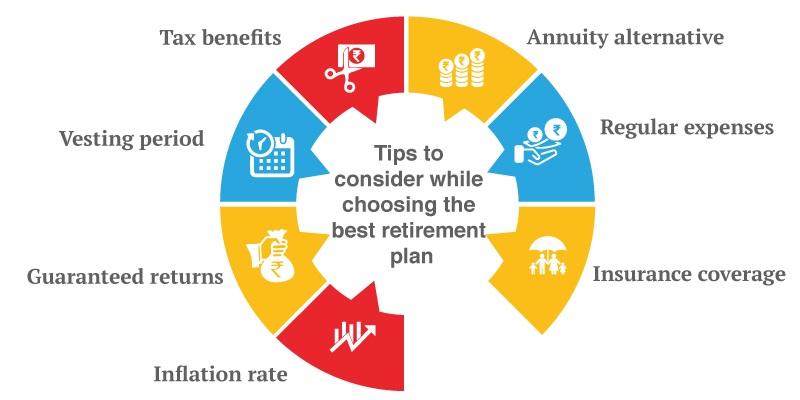

The best kind of account for you will depend on several things, such as your long-term financial objectives, work status, and present tax situation. You may maximize your retirement savings strategy by navigating these possibilities with the assistance of a financial advisor.

Projecting Your Retirement Income

Creating realistic projections for your retirement income is crucial to ensuring financial stability. Consider all potential income sources, including social security, pensions, and withdrawals from retirement accounts. Tools like retirement calculators can provide valuable insights into future financial scenarios and help you adjust your savings strategy accordingly.

Social Security benefits are often a significant component of retirement income. Understanding how your benefits are calculated and knowing the best time to claim them can substantially impact your financial health. Although less common today, pensions also require careful planning to meet your retirement needs.

Managing your withdrawals from retirement accounts, such as 401(k)s and IRAs, is important to reduce your tax obligations and ensure your assets last throughout retirement. You can prevent outliving your investments by using conservative withdrawal methods and realistic growth rates.

Planning for Retirement Expenses

Accurately estimating your retirement expenses is another pivotal step in retirement planning. Typical expenses include:

- As you get older, healthcare bills usually go up dramatically. It is critical to factor in premiums, co-pays, and out-of-pocket costs for therapies that Medicare does not cover.

- Housing, whether you own your home outright or plan to downsize. Consider property taxes, maintenance, and potential mortgage payments if you still need to pay off your house.

- Leisure activities, hobbies, and travel that you plan to enjoy during retirement. Allocating funds for these activities ensures you can enjoy retirement without financial strain.

Using historical data and adjusting for inflation will give you a more precise estimate of future expenses. It’s also wise to build a buffer into your budget for unexpected costs, such as major home repairs or unplanned medical expenses.

Managing and Adjusting Your Retirement Plan

Flexibility is critical to a successful retirement plan. Regularly reviewing your plan and adjusting as needed ensures you stay on track. Financial experts advise conducting a yearly review of your retirement plan, which includes assessing your investment performance and reassessing your retirement goals.

Additionally, keeping abreast of changes in tax laws and retirement account regulations is crucial. These changes can affect your savings and withdrawal strategies, making it essential to update your plan accordingly.

Life events such as marriage, divorce, or a significant health issue can also necessitate adjustments to your retirement plan. Being proactive in managing these changes helps you maintain your financial stability.

Fractional Accounting by Precise Management provides high quality financial management including book keeping, financial reporting and compliance helping with your business growth objective.

Common Mistakes to Avoid

Avoiding common pitfalls can protect your retirement plans. Some mistakes include:

- Underestimating future expenses, especially healthcare costs.

- Relying too heavily on one income source can be risky if that source becomes unstable.

- You need to diversify your investments and increase your exposure to market volatility.

- Refrain from maintaining an emergency fund, which can cover unexpected expenses without derailing your retirement plans.

By being aware of these potential issues, you can take proactive steps to mitigate their impact on your retirement. Regularly updating your financial knowledge and consulting with professionals can help avoid these common mistakes.

Read More: Understanding Venture Debt